As filed with the U.S. Securities and Exchange Commission on June 16, 2021

Registration No. 333-256405

DELAWARE | | | 5961 | | | 83-4284557 |

(STATE OR OTHER JURISDICTION OF INCORPORATION OR ORGANIZATION) | | | (PRIMARY STANDARD INDUSTRIAL CLASSIFICATION CODE NUMBER) | | | (I.R.S. EMPLOYER IDENTIFICATION NUMBER) |

Louis Lombardo, Esq. Denis Dufresne, Esq. Agatha Rysinski, Esq. Meister Seelig & Fein LLP 125 Park Avenue, 7th Floor New York, New York 10017 Tel: (212) 655-3500 Fax: (212) 655-3535 | | | Nolan Taylor, Esq. David Marx, Esq. Dorsey & Whitney, LLP 111 South Main Street, Suite 2100 Salt Lake City, Utah 84111 Tel: (801) 933-7360 Fax: (801) 933-7373 |

Large accelerated filer | | | ☐ | | | Accelerated filer | | | ☐ |

Non-accelerated filer | | | ☒ | | | Smaller reporting company | | | ☒ |

| | | | | Emerging growth company | | | ☐ |

Title of Each Class of Securities to be Registered | | | Proposed Maximum Aggregate Offering Price(1) | | | Amount of Registration Fee(2) |

Common Stock, $0.001 par value share | | | $40,500,000 | | | $4,418.55 |

(1) | Estimated solely for the purpose of computing the amount of the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended. |

(2) | Calculated pursuant to Rule 457(o) based on an estimate of the proposed maximum offering price. The registrant previously paid a total of $5,545 in connection with the previous filing of the registration statement. |

| | | Per Share | | | Total | |

Public offering price | | | $ | | | $ |

Underwriting discounts and commissions(1) | | | $ | | | $ |

Proceeds to us (before expenses) | | | $ | | | $ |

(1) | See section titled “Underwriting” for a description of the compensation payable to the underwriters. |

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | |

• | the impact of COVID-19 on the U.S. and global economies, our employees, suppliers, customers and end consumers, which could adversely and materially impact our business, financial condition and results of operations |

• | our ability to successfully implement our growth strategy; |

• | failure to achieve growth or manage anticipated growth; |

• | our ability to achieve or maintain profitability; |

• | our significant indebtedness; |

• | the loss of key members of our senior management team; |

• | our ability to generate sufficient cash flow or raise capital on acceptable terms to run our operations, service our debt and make necessary capital expenditures; |

• | our ability to maintain effective internal control over financial reporting; |

• | our limited operating history; |

• | our ability to successfully integrate Halo’s and TruPet’s businesses and realize anticipated benefits with these acquisitions and with other acquisitions or investments we may make; |

• | our dependence on our subsidiaries for payments, advances and transfers of funds due to our holding company status; |

• | our ability to successfully develop additional products and services or successfully market and commercialize such products and services; |

• | competition in our market; |

• | our ability to attract new and retain existing customers, suppliers, distributors or retail partners; |

• | allegations that our products cause injury or illness or fail to comply with government regulations; |

• | our ability to manage our supply chain effectively; |

• | our or our third-party contract manufacturers’ and suppliers’ ability to comply with legal and regulatory requirements; |

• | the effect of potential price increases and shortages on the inputs, commodities and ingredients that we require; |

• | our ability to develop and maintain our brand and brand reputation; |

• | compliance with data privacy rules; |

• | our compliance with applicable regulations issued by the U.S. Food and Drug Administration (“FDA”), the U.S. Federal Trade Commission (“FTC”), the U.S. Department of Agriculture (“USDA”), and other federal, state and local regulatory authorities, including those regarding marketing pet food, products and supplements; |

• | risk of our products being recalled for a variety of reasons, including product defects, packaging safety and inadequate or inaccurate labeling disclosure; |

• | risk of shifting customer demand in relation to raw pet foods, premium kibble and canned pet food products, and failure to respond to such changes in customer taste quickly and effectively; and |

• | the other risks identified in this prospectus including, without limitation, those under “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” as such factors may updated from time to time in our other filings with the SEC. |

• | Portfolio of Established Premium and Super-Premium Pet Brands With a History of Success. We believe that both the Halo and Trudog brands are well positioned to take advantage of pet parents’ increasing desire to feed only the highest quality ingredients to their pets, and that there will continue to be innovative opportunities for brand consolidation over time. Today, the Halo and TruDog brands are focused on serving consumers in the United States, Canada and select Asian markets including China. |

• | Online Recurring Revenue Represents Significant Percentage of Total Sales. We believe that customers who purchase products on a monthly subscription tend to be high value, long-term customers. In order to increase the number of customers that subscribe to purchase our products, we offer incentives alongside our E-Commerce partners, which often take the form of a discounted initial subscription order and a small discount on each subsequent purchase. In the first quarter of 2021, 63% of end-consumer sales on Chewy were placed by subscribers, 39% of end-consumer sales on Amazon were placed by subscribers and 48% of DTC sales made on our website were placed by subscribers. In the aggregate, more than 30% of Better |

• | Exposure to Fastest Growing Sub-Sectors of Premium Pet. Freeze-dried raw dog food is one of the fastest growing sub-categories of premium pet food, with Packaged Facts reporting 39% year-over-year growth in the sub-category in 2019. According to Packaged Facts’ March 2020 Consumer Survey, 4% of pet owners are using vegetarian formulations, with a growing percentage of consumers focused on ingredients that are sustainably sourced and utilized. We believe we are well positioned to take advantage of these growing sub-sectors through Halo’s successful line of freeze-dried treats for dogs and cats and a growing line of award-winning vegan products for dogs and TruDog’s ultra-premium, freeze-dried raw dog food, which represents a majority of its sales. |

• | Asset Light Model with Established Long Term Co-Manufacturing Partners. Our products are manufactured by an established network of co-manufacturers in partnership with Better Choice. The Company has maintained each of its key co-packing relationships for more than four years, with certain relationships in place for more than 10 years. Four co-manufactures account for more than 95% of our food and treat related purchases and all of our products are co-manufactured in the United States. Our products meet stringent requirements to ensure compliance with required and voluntary regulatory groups, including AAFCO, the Marine Stewardship Council (MSC) and the Global Animal Partnership (GAP). In addition, we constantly evaluate the capabilities of our co-manufactures to ensure continuity of supply in addition to holding what we believe are sufficient safety stocks of product on hand in the event of supply chain disruptions. |

• | Rapidly Growing International Presence. In 2020, the Halo brand achieved $8.6 million in sales, representing 95% growth year-over-year. We believe that growth in Asia is fueled by increasing levels of economic financial status and demand for premium and super-premium, western manufactured products, with our sales currently concentrated in the high growth markets of China, Korea, Japan and Taiwan. |

• | Key Competitive Advantages in Chinese Market. In 2020, 48% of our international sales were made in China. We believe several factors give us an advantage in China relative to our competition, including that (1) we have secured approval from the Chinese Ministry of Agriculture to sell 15 dry diets in mainland China, which is typically a multi-year process for first-time applicants; (2) we have a multi-year distribution partner in Penefit, with a dedicated team of more than 20 individuals in-country that are focused solely on selling the Halo brand; and (3) we have established supply chain partners with whitelisted approval to import product. |

• | Executive Team Purpose Built for Success in Pet Industry. Our executive team has over 50 years of combined experience in the Pet Industry, and has led multiple brands, such as Nutro, Merrick and Solid Gold, to successful exits. |

• | Strong Innovation Pipeline. We have a robust and growing pipeline of new products, and believe our size is an advantage – we are nimble enough to quickly bring new products to market, but large enough to benefit from strong existing customer relationships and established economies of scale with our co-manufacturers. Most notably, in 2022 we plan to introduce a new Halo sub-brand for pet specialty stores, an update to our existing Halo Holistic sub-brand and an expansion of our vegan and freeze-dried lines. |

• | Ability to Leverage Differentiated Omni-Channel Strategy for Growth. We believe that we can leverage our differentiated omni-channel strategy to design and sell products purpose-built for success in specific channels while maintaining our ability to leverage marketing and sales resources cross-channel. We believe that this strategy will allow us to deliver on core consumer needs, maximize gross margin and respond to changing channel dynamics that have accelerated because of the COVID-19 pandemic. For example, we can take learnings from the online environment, which represented 59% of our 2020 sales, to the offline environment, which we see as poised for growth at pet specialty stores in 2022. This approach will be under a single banner brand, Halo. |

• | Capitalize on continuing trends of pet humanization. We believe our combination of innovative products designed specifically for certain channels can assist our growth to become a leader in the premium and super-premium categories across dog and cat food. With an average of more than $500 spent annually on pet food per pet owning household and the number of pet owning households increasing, we believe that the super-premium sub-category is poised to be among the fastest growing segments of pet care spending. |

• | Well Positioned to Capitalize On a Once-in-a-Generation Demographic Shift in China. We believe that China represents the largest macro-growth opportunity in the global pet food industry. In China, the number of households that own a pet has doubled in the last five years, with younger pet owners leading growth. Even though the absolute number of Chinese households that own a pet recently surpassed that same figure in the US, only 20% of Chinese households own a pet, compared to 67% in the United States. This has translated to a 28% annual growth rate in the premium dry cat food market, and a 20% annual growth rate in the dry dog food market. In 2020, more than 50% of Chinese consumers that purchased our products were born after 1990, and approximately 80% made those purchases online. |

• | Ability to Pursue Strategic Acquisitions. In 2019, we successfully closed the Halo and TruPet acquisitions. We remain committed to locating the right assets that meet our investment criteria. Through our longstanding industry contacts we are able to source proprietary opportunities and transactions. Our preference is to maintain the asset light business model we currently operate and identify products and brands that are complementary to our existing portfolio. We have a wide scope of systems in place to ensure scalable success and reduce integration risk, including a world class enterprise resource planning or ERP system, NetSuite, a fully scaled and outsourced IT provider (Chelsea Technologies) and a platform to effectively meet public company reporting requirements (Workiva). Furthermore, our public company structure has historically enabled Better Choice to offer transaction consideration in the form of cash and stock. We have a robust pipeline of potential acquisitions which we expect to pursue in the form of pre-process and direct founder dialogue discussions. |

• | We have a history of losses, we expect to incur losses in the future and we may not be able to achieve or maintain profitability which may affect our ability to continue as a going concern; |

• | The COVID-19 pandemic could have a material adverse impact on our business, results of operations and financial condition; |

• | We may not be able to successfully implement our growth strategy or effectively manage our growth on a timely basis or at all; |

• | Our level of indebtedness and related covenants could limit our operational and financial flexibility and significant adversely affect our business if we breach such covenants and default on such indebtedness; |

• | If we do not successfully develop additional products and services, or if such products and services are developed but not successfully commercialized, our business will be adversely affected; |

• | Our ability to compete on the basis of product and ingredient quality, product availability, palatability, brand awareness, loyalty and trust, product variety and innovation, product packaging and design, reputation, price and convenience and promotional efforts in our highly competitive industry and against other industry participants, some of whom have greater resources than we do; |

• | We are vulnerable to fluctuations in the price and supply of key inputs, including ingredients, packaging materials, and freight; |

• | Food safety and food-borne illness incidents may materially adversely affect our business by exposing us to lawsuits, product recalls or regulatory enforcement actions, increasing our operating costs and reducing demand for our product offerings; |

• | Interruption in our sourcing operations could disrupt production, shipment or receipt of our merchandise, which would result in lost sales and could increase our costs; |

• | We depend on the knowledge and skills of our senior management and other key employees, and if we are unable to retain and motivate them or recruit additional qualified personnel, our business may suffer; |

• | We rely heavily on third-party commerce platforms to conduct our businesses and if one of those platforms is compromised, our business, financial condition and results of operations could be harmed; |

• | Adverse litigation judgments or settlements resulting from legal proceedings relating to our business operations could materially adversely affect our business, financial condition and results of operations; |

• | International expansion of our business, particularly into China, could expose us to substantial business, regulatory, political, financial and economic risks; |

• | Changes in existing laws or regulations, including how such existing laws or regulations are enforced by federal, state, and local authorities, or the adoption of new laws or regulations may increase our costs and otherwise adversely affect our business, financial condition and results of operations; |

• | There is currently a limited public market for our common stock, a trading market for our common stock may never develop, and our common stock prices may be volatile and could decline substantially; |

• | The reverse stock split may not achieve the requisite increase in the market price for our common stock to continue to comply with listing requirements of the NYSE American and may decrease the liquidity of the shares of our common stock; |

• | Provisions in our certificate of incorporation and bylaws and Delaware law may discourage a takeover attempt even if a takeover might be beneficial to our stockholders; and |

• | We have broad discretion in the use of the net proceeds from this offering, and our use of those proceeds may not yield a favorable return on your investment. |

• | 10,062,363 shares of our common stock issuable upon the exercise of warrants to purchase our common stock as of June 11, 2021, at a weighted-average exercise price of $7.14 per share; and |

• | 2,207,704 shares of our common stock issuable upon the exercise of stock options outstanding as of June 11, 2021, at a weighted average exercise price of $6.42 per share and 42,297 shares of our common stock reserved for future issuance under our Amended and Restated 2019 Incentive Award Plan. |

| | | For the Three Months Ended | | | For the Year Ended | |||||||

| | | March 31, 2021 | | | March 31, 2020 | | | December 31, 2020 | | | December 31, 2019 | |

Net sales | | | $10,830 | | | $12,226 | | | $42,590 | | | $15,577 |

Cost of goods sold | | | $6,556 | | | $8,069 | | | $26,491 | | | $9,717 |

Gross profit | | | $4,274 | | | $4,157 | | | $16,099 | | | $5,860 |

Operating expenses | | | $9,412 | | | $12,689 | | | $43,421 | | | $42,186 |

Loss from operations | | | $(5,138) | | | $(8,532) | | | $(27,322) | | | $(36,326) |

Other expense, net | | | $7,712 | | | $922 | | | $32,013 | | | $148,136 |

Net and comprehensive loss | | | $(12,850) | | | $(9,454) | | | $(59,335) | | | $(184,462) |

Preferred dividends | | | — | | | $34 | | | $103 | | | $109 |

Net and comprehensive loss available to common stockholders | | | $(12,850) | | | $(9,488) | | | $(59,438) | | | $(184,571) |

Weighted average number of shares outstanding, basic and diluted | | | 9,587,509 | | | 8,087,733 | | | 8,180,739 | | | 5,539,767 |

Loss per share, basic and diluted(1) | | | $(1.38) | | | $(1.17) | | | $(7.26) | | | $(33.32) |

| | | | | | | | | |||||

Pro forma loss per share, basic and diluted (unaudited)(1)(2) | | | $(0.73) | | | | | $(3.55) | | | ||

Weighted average number of shares outstanding used to compute pro forma net loss per share, basic and diluted (unaudited)(2) | | | 18,119,481 | | | | | 16,712,711 | | | ||

(1) | The calculation of loss per share and pro forma loss per share for the three months ended March 31, 2021 and for the year ended December 31, 2020 includes certain adjustments to the net and comprehensive loss for items directly impacting accumulated deficit. See “Note 15 – Net loss per share” to our unaudited condensed consolidated financial statements for the period ended March 31, 2021 included in this prospectus and “Note 20 – Net loss per share” to our audited consolidated financial statements for the year ended December 31, 2020 included in this prospectus for more information. |

(2) | Pro forma net loss per share gives effect to the automatic conversion of all of our outstanding shares of Series F Preferred Stock into 5,768,517 shares of common stock as of March 31, 2021 as well as the automatic conversion of our outstanding convertible notes into 2,763,455 shares of common stock as of March 31, 2021. |

| | | March 31, 2021 | | | December 31, 2020 | | | December 31, 2019 | |

Total Current Assets | | | $19,876 | | | $17,563 | | | $17,579 |

Total Assets | | | $52,367 | | | $51,253 | | | $53,532 |

Total Current Liabilities | | | $55,065 | | | $54,576 | | | $33,026 |

Total Liabilities | | | $85,347 | | | $79,355 | | | $50,037 |

Redeemable Series E Preferred Stock | | | — | | | — | | | $10,566 |

Total Stockholders’ Deficit | | | $(32,980) | | | $(28,102) | | | $(7,071) |

| | | Three Months Ended | | | Year Ended | ||||

| | | March 31, 2021 | | | March 31, 2020 | | | December 31, 2020 | |

Net and comprehensive loss available to common stockholders | | | $(12,850) | | | $(9,488) | | | $(59,438) |

Depreciation and amortization | | | 411 | | | 457 | | | 1,748 |

Interest expense | | | 835 | | | 2,301 | | | 9,247 |

EBITDA | | | $(11,604) | | | $(6,730) | | | $(48,443) |

Non-cash share-based compensation, warrant expense and dividends(a) | | | $2,590 | | | $5,113 | | | $19,175 |

Non-cash change in fair value of warrant liability and warrant derivative liability | | | 6,483 | | | (1,379) | | | 22,678 |

Loss on extinguishment of debt | | | 394 | | | — | | | $88 |

Acquisition related expenses/(income)(b) | | | — | | | 677 | | | (150) |

Non-cash effect of purchase accounting and inventory write-off on cost of goods sold(c) | | | — | | | 894 | | | 1,111 |

Offering related expenses(d) | | | 196 | | | 315 | | | 1,221 |

Non-recurring expenses(e) | | | 856 | | | 982 | | | 2,351 |

COVID-19 expenses(f) | | | — | | | — | | | $30 |

Adjusted EBITDA | | | $(1,085) | | | $(128) | | | $(1,939) |

(a) | Reflects non-cash expenses related to equity compensation awards and stock purchase warrants. The periods in 2020 additionally include non-cash dividends and stock purchase warrants associated with a contract that was subsequently terminated. Share-based compensation is |

(b) | Reflects costs incurred related to acquisition and integration activities that will not recur and operating expenses that will not recur due to acquisition related synergies. |

(c) | Reflects non-cash expense recognized in cost of goods sold related to the step-up of inventory required under the accounting rules for business combinations ($0.9 million); and non-cash write off of expired CBD inventory ($0.2 million). |

(d) | Reflects administrative costs associated with the registration of previously issued common shares and other debt and equity financing transactions. |

(e) | Reflects non-recurring severance costs ($0.7 million), non-cash third party share-based compensation ($0.3m), non-recurring consulting costs ($0.2 million) and director costs ($0.1 million), partially offset by a $0.5 million reduction to sales tax liability for the three months ended March 31, 2021. Reflects contract termination costs ($1.0 million) for the three months ended March 31, 2020; additionally includes write off of a prepaid asset related to the termination of a contract entered into during 2019 ($0.4 million), non-recurring consulting costs ($0.3 million), non-cash loss on disposal of assets ($0.2 million), and other non-recurring costs for the year ended December 31, 2020. |

(f) | Reflects cleaning, sanitizing, protective equipment and hazard compensation related to COVID-19. |

• | the inability to integrate the respective businesses of Bona Vida, Halo and TruPet in a manner that permits the combined business to achieve the synergies anticipated to result from the acquisitions, which could result in the anticipated benefits of the acquisitions not being realized partly or wholly in the time frame currently anticipated or at all; |

• | integrating personnel from the three companies while maintaining focus on safety and providing consistent, high quality products and customer service; and |

• | performance shortfalls at one or all of the companies as a result of the diversion of management's attention caused by the acquisitions and integrating the companies' operations. |

• | the effectiveness and efficiency of our online experience for disparate worldwide audiences, including advertising and search optimization programs in generating consumer awareness and sales of our products; |

• | our ability to prevent confusion among consumers that can result from search engines that allow competitors to use or bid on our trademarks to direct consumers to competitors’ websites; |

• | our ability to prevent Internet publication or television broadcast of false or misleading information regarding our products or our competitors’ products; |

• | the nature and tone of consumer sentiment published on various social media sites; and |

• | the stability of our website and other e-commerce platforms we sell our products on. In recent years, a number of DTC, Internet-based retailers have emerged and have driven up the cost of basic search terms, which has and may continue to increase the cost of our Internet-based marketing programs. |

• | political, social and economic instability; |

• | higher levels of credit risk, corruption and payment fraud; |

• | regulations that might add difficulties in repatriating cash earned outside the United States and otherwise prevent us from freely moving cash; |

• | import and export controls and restrictions and changes in trade regulations; |

• | compliance with the U.S. Foreign Corrupt Practices Act, the U.K. Bribery Act and similar laws in other jurisdictions; |

• | multiple, conflicting and changing laws and regulations such as privacy, security and data use regulations, tax laws, trade regulations, economic sanctions and embargoes, employment laws, anticorruption laws, regulatory requirements, reimbursement or payor regimes and other governmental approvals, permits and licenses; |

• | failure by us, our collaborators or our distributors to obtain regulatory clearance, authorization or approval for the use of our products in various countries; |

• | additional potentially relevant third-party patent rights; |

• | complexities and difficulties in obtaining intellectual property protection and enforcing our intellectual property; |

• | logistics and regulations associated with shipping samples and customer orders, including infrastructure conditions and transportation delays; |

• | the impact of local and regional financial crises; |

• | natural disasters, political and economic instability, including wars, terrorism and political unrest, and outbreak of disease; |

• | breakdowns in infrastructure, utilities and other services; |

• | boycotts, curtailment of trade and other business restrictions; and |

• | the other risks and uncertainties described in this prospectus. |

• | We will indemnify our directors and officers for serving us in those capacities or for serving other business enterprises at our request, to the fullest extent permitted by Delaware law. Delaware law provides that a corporation may indemnify such person if such person acted in good faith and in a manner such person reasonably believed to be in or not opposed to the best interests of the corporation and, with respect to any criminal action or proceeding, had no reasonable cause to believe such person’s conduct was unlawful. |

• | We may, in our discretion, indemnify employees and agents in those circumstances where indemnification is permitted by applicable law. |

• | We are required to advance expenses, as incurred, to our directors and officers in connection with defending a proceeding, except that such directors or officers shall undertake to repay such advances if it is ultimately determined that such person is not entitled to indemnification. |

• | We will not be obligated pursuant to the indemnification agreements entered into with our directors and executive officers to indemnify a person with respect to proceedings initiated by that person, except with respect to proceedings to enforce an indemnitees right to indemnification or advancement of expenses, proceedings authorized by our board of directors and if offered by us in our sole discretion. |

• | The rights conferred in our certificate of incorporation are not exclusive, and we are authorized to enter into indemnification agreements with our directors, officers, employees and agents and to obtain insurance to indemnify such persons. |

• | We may not retroactively amend our certificate of incorporation or indemnification agreement provisions to reduce our indemnification obligations to directors, officers, employees and agents. |

| | | High | | | Low | |

2019 | | | | | ||

First Quarter(1) | | | $79.56 | | | $7.98 |

Second Quarter(1) | | | $54.90 | | | $20.40 |

Third Quarter(1) | | | $38.76 | | | $18.72 |

Fourth Quarter(1) | | | $26.10 | | | $7.86 |

2020 | | | | | ||

First Quarter(1) | | | $16.20 | | | $3.00 |

Second Quarter(1) | | | $12.00 | | | $3.60 |

Third Quarter(1) | | | $12.00 | | | $1.44 |

Fourth Quarter(2) | | | $7.68 | | | $2.70 |

2021 | | | | | ||

First Quarter(3) | | | $10.80 | | | $6.84 |

(1) | The high and low bid prices for this quarter were reported by the OTCQB marketplace. |

(2) | The high and low bid prices for this quarter were reported by the OTCQB & OTCQX marketplaces. |

(3) | The high and low bid prices for this quarter were reported by the OTCQX marketplace. |

• | an actual basis (as adjusted for the reverse stock split of 1-for-6); and |

• | on a pro forma basis (as adjusted for the reverse stock split of 1-for-6) to reflect, based on an assumed offering price of $9.00 per share of common stock, (i) the issuance of 5,768,517 shares of our common stock upon the conversion of all of the shares of Series F Preferred Stock outstanding as of March 31, 2021 and (ii) the issuance of 2,763,455 shares of common stock upon conversion of our outstanding convertible notes, based upon the terms of the outstanding convertible notes as of March 31, 2021; and |

• | on a pro forma as adjusted basis to give effect to the sale and issuance of 4,500,000 shares of common stock offered by us in this offering, based on the assumed public offering price of $9.00 per share, after deducting the underwriting discounts and commissions and estimated offering expenses. |

| | | As of March 31, 2021 | |||||||

In thousands (except shares) | | | Actual | | | Pro Forma | | | Pro Forma As Adjusted(1) |

Cash and cash equivalents | | | $4,298 | | | $4,298 | | | $41,163 |

| | | | | | | ||||

Long-term debt, including current maturities: | | | | | | | |||

Loans and line of credit, net | | | $10,628 | | | $10,628 | | | $10,628 |

Notes payable, net | | | $19,609 | | | $— | | | $— |

PPP Loans | | | $852 | | | $852 | | | $852 |

Total debt, net of debt issuance costs and discounts | | | $31,089 | | | $11,480 | | | $11,480 |

Warrant Liability | | | $46,333 | | | $— | | | $— |

| | | | | | | ||||

Stockholders’ Deficit: | | | | | | | |||

Common stock, $0.001 par value, 200,000,000 shares authorized | | | $11 | | | $20 | | | $24 |

Series F Preferred Stock, $0.001 par value, 30,000 shares authorized | | | $— | | | $— | | | $— |

Additional paid-in capital | | | $240,902 | | | $308,305 | | | $345,166 |

Accumulated deficit | | | $(273,893) | | | $(275,363) | | | $(275,363) |

Total stockholders’ (deficit) equity | | | $(32,980) | | | $32,962 | | | $69,827 |

Total capitalization | | | $44,442 | | | $44,442 | | | $81,307 |

(1) | Each $1.00 increase or decrease in the assumed public offering price of $9.00 per share would increase or decrease, as applicable, the net proceeds to us from the sale of shares of our common stock in this offering by $4.2 million, assuming that the number of shares offered by us, as set forth on the cover page of this prospectus, remains the same (assuming no exercise of the underwriter’s over-allotment option) and after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us. Similarly, each increase or decrease of 500,000 shares in the number of shares offered by us would increase or decrease, as applicable, the net proceeds to us from the sale of shares of our common stock in this offering by approximately $4.2 million, assuming the assumed public offering price of $9.00 remains the same and after deducting underwriting discounts and commissions and estimated offering expenses payable by us. |

• | 2,191,812 shares of our common stock issuable upon the exercise of stock options outstanding as of March 31, 2021, at a weighted average exercise price of $6.36 per share; |

• | 10,145,697 shares of our common stock issuable upon the exercise of warrants outstanding as of March 31, 2021, at a weighted average exercise price of $7.08 per share; and |

• | 58,188 shares of our common stock reserved for future issuance under our Amended and Restated 2019 Equity Incentive Plan as well as any automatic increases in the number of shares of our common stock reserved for future issuance under our plan. |

Assumed public offering price per share | | | | | $9.00 | |

Net tangible book deficit per share as of March 31, 2021 | | | $ | | | (5.85) |

Pro forma net tangible book value per share as of March 31, 2021 including the conversion of Series F Preferred Stock and notes payable before this offering | | | | | $0.08 | |

Increase in net tangible book value per share attributable to this offering | | | | | $1.52 | |

Pro forma net tangible book value per share after the offering | | | $1.60 | | | |

Dilution per share to new investors participating in the offering | | | | | $7.40 |

• | 2,191,812 shares of our common stock issuable upon the exercise of stock options outstanding as of March 31, 2021, at a weighted average exercise price of $6.36 per share; |

• | 10,145,697 shares of our common stock issuable upon the exercise of warrants outstanding as of March 31, 2021, at a weighted average exercise price of $7.08 per share; and |

• | 58,188 shares of our common stock reserved for future issuance under our Amended and Restated 2019 Equity Incentive Plan as well as any automatic increases in the number of shares of our common stock reserved for future issuance under our plan. |

| | | Three Months Ended March 31, | | | | | ||||||

| | | 2021 | | | 2020 | | | Change | | | % | |

Net sales | | | $10,830 | | | $12,226 | | | $(1,396) | | | (11)% |

Cost of goods sold | | | 6,556 | | | 8,069 | | | (1,513) | | | (19)% |

Gross profit | | | $4,274 | | | $4,157 | | | $117 | | | 3% |

Operating expenses: | | | | | | | | | ||||

General and administrative | | | $4,551 | | | $8,246 | | | $(3,695) | | | (45)% |

Share-based compensation | | | 2,525 | | | 2,484 | | | 41 | | | 2% |

Sales and marketing | | | 2,336 | | | 1,959 | | | 377 | | | 19% |

Total operating expenses | | | $9,412 | | | $12,689 | | | $(3,277) | | | (26)% |

Loss from operations | | | $(5,138) | | | $(8,532) | | | $3,394 | | | (40)% |

| | | Three Months Ended March 31, | ||||||||||

| | | 2021 | | | 2020 | |||||||

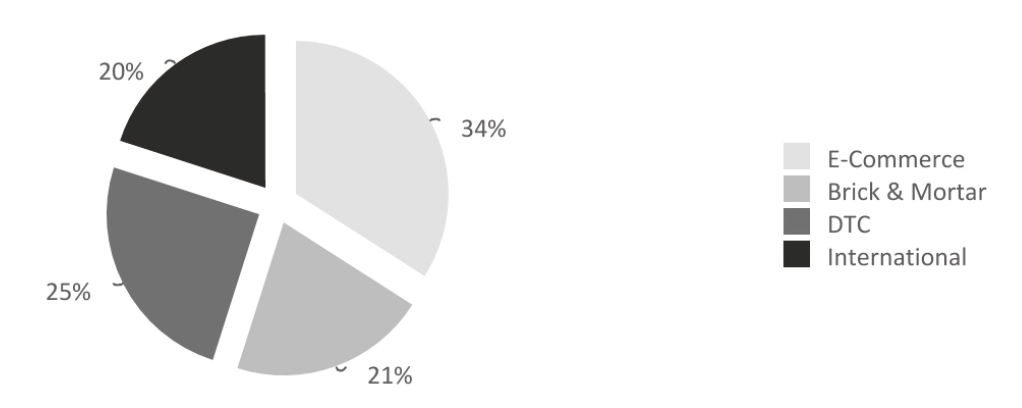

E-commerce | | | $4,010 | | | 37% | | | $4,481 | | | 37% |

Brick & Mortar | | | 1,894 | | | 18% | | | 2,897 | | | 23% |

DTC | | | 2,436 | | | 22% | | | 2,804 | | | 23% |

International | | | 2,490 | | | 23% | | | 2,044 | | | 17% |

Net Sales | | | $10,830 | | | 100% | | | $12,226 | | | 100% |

| | | Years Ended December 31, | | | Change | |||||||

| | | 2020 | | | 2019 | | | $ | | | % | |

Net sales | | | $42,590 | | | $15,577 | | | $27,013 | | | 173% |

Cost of goods sold | | | 26,491 | | | 9,717 | | | 16,774 | | | 173% |

Gross profit | | | 16,099 | | | 5,860 | | | 10,239 | | | 175% |

Operating expenses: | | | | | | | | | ||||

General and administrative | | | 26,589 | | | 20,879 | | | 5,710 | | | 27% |

Share-based compensation | | | 8,940 | | | 10,280 | | | (1,340) | | | (13)% |

Sales and marketing | | | 7,892 | | | 10,138 | | | (2,246) | | | (22)% |

Impairment of intangible asset | | | — | | | 889 | | | (889) | | | (100)% |

Total operating expenses | | | 43,421 | | | 42,186 | | | 1,235 | | | 3% |

Loss from operations | | | $(27,322) | | | $(36,326) | | | $9,004 | | | (25)% |

| | | Years Ended December 31, | ||||||||||

| | | 2020 | | | 2019 | |||||||

E-commerce | | | $14,218 | | | 34% | | | $1,952 | | | 13% |

Brick & Mortar | | | 8,982 | | | 21% | | | 194 | | | 1% |

DTC | | | 10,778 | | | 25% | | | 13,392 | | | 86% |

International | | | 8,612 | | | 20% | | | 39 | | | —% |

Net Sales | | | $42,590 | | | 100% | | | $15,577 | | | 100% |

| | | Three Months Ended March 31, | | | Year Ended December 31, | |||||||

| | | 2021 | | | 2020 | | | 2020 | | | 2019 | |

Cash flows (used in) provided by: | | | | | | | | | ||||

Operating activities | | | $(2,325) | | | $(1,159) | | | $(7,505) | | | $(20,969) |

Investing activities | | | — | | | (8) | | | (151) | | | (20,207) |

Financing activities | | | 2,697 | | | 500 | | | 9,111 | | | 39,764 |

Net increase (decrease) in cash and cash equivalents | | | $372 | | | $(667) | | | $1,455 | | | $(1,412) |

• | Portfolio of Established Premium and Super-Premium Pet Brands With a History of Success. We believe that both the Halo and Trudog brands are well positioned to take advantage of pet parents’ increasing desire to feed only the highest quality ingredients to their pets, and that there will continue to be innovative opportunities for brand consolidation over time. Today, the Halo and TruDog brands are focused on serving consumers in the United States, Canada and select Asian markets including China. |

• | Online Recurring Revenue Represents Significant Percentage of Total Sales. We believe that customers who purchase products on a monthly subscription tend to be high value, long-term customers. In order to increase the number of customers that subscribe to purchase our products, we offer incentives alongside our E-Commerce partners, which often take the form of a discounted initial subscription order and a small discount on each subsequent purchase. In the first quarter of 2021, 63% of end-consumer sales on Chewy were placed by subscribers, 39% of end-consumer sales on Amazon were placed by subscribers and 48% of DTC sales made on our website were placed by subscribers. In the aggregate, more than 30% of Better Choice’s total sales in the first quarter of 2021 can be attributed to end-customer subscription. According to Packaged Facts, roughly one third of pet food purchases made online were placed via subscription, indicating that this is a relative competitive strength. |

• | Exposure to Fastest Growing Sub-Sectors of Premium Pet. Freeze-dried raw dog food is one of the fastest growing sub-categories of premium pet food, with Packaged Facts reporting 39% year-over-year growth in the sub-category in 2019. According to Packaged Facts’ March 2020 Consumer Survey, 4% of pet owners are using vegetarian formulations, with a growing percentage of consumers focused on ingredients that are sustainably sourced and utilized. We believe we are well positioned to take advantage of these growing sub-sectors through Halo’s successful line of freeze-dried treats for dogs and cats and a growing line of award-winning vegan products for dogs and TruDog’s ultra-premium, freeze-dried raw dog food, which represents a majority of its sales. |

• | Asset Light Model with Established Long Term Co-Manufacturing Partners. Our products are manufactured by an established network of co-manufacturers in partnership with Better Choice. The Company has maintained each of its key co-packing relationships for more than four years, with certain relationships in place for more than 10 years. Four co-manufactures account for more than 95% of our food and treat related purchases and all of our core products are co-manufactured in the United States. Our products meet stringent requirements to ensure compliance with required and voluntary regulatory groups, including AAFCO, the Marine Stewardship Council (MSC) and the Global Animal Partnership (GAP). In addition, we constantly evaluate the capabilities of our co-manufactures to ensure continuity of supply in addition to holding what we believe are sufficient safety stocks of product on hand in the event of supply chain disruptions. |

• | Rapidly Growing International Presence. In 2020, the Halo brand achieved $8.6 million in sales, representing 95% growth year-over-year. We believe that growth in Asia is fueled by increasing levels of economic financial status and demand for premium and super-premium, western manufactured products, with our sales currently concentrated in the high growth markets of China, Korea, Japan and Taiwan. |

• | Key Competitive Advantages in Chinese Market. In 2020, 48% of our international sales were made in China. We believe several factors give us an advantage in China relative to our competition, including that (1) we have secured approval from the Chinese Ministry of Agriculture to sell 15 dry diets in mainland China, which is typically a multi-year process for first time applicants; (2) we have a multi-year distribution partner in Penefit, with a dedicated team of more than 20 individuals in-country that are focused solely on selling the Halo brand; and (3) we have established supply chain partners with whitelisted approval to import product. |

• | Executive Team Purpose Built for Success in Pet Industry. Our executive team has over 50 years of combined experience in the Pet Industry, and has led multiple brands, such as Nutro, Merrick and Solid Gold, to successful exits. |

• | Strong Innovation Pipeline. We have a robust and growing pipeline of new products, and believe our size is an advantage – we are nimble enough to quickly bring new products to market, but large enough to benefit from strong existing customer relationships and established economies of scale with our co-manufacturers. Most notably, in 2022 we plan to introduce a new Halo sub-brand for pet specialty stores, an update to our existing Halo Holistic sub-brand and an expansion of our vegan and freeze-dried lines. |

• | Ability to Leverage Differentiated Omni-Channel Strategy for Growth. We believe that we can leverage our differentiated omni-channel strategy to design and sell products purpose-built for success in specific channels while maintaining our ability to leverage marketing and sales resources cross-channel. We believe that this strategy will allow us to deliver on core consumer needs, maximize gross margin and respond to changing channel dynamics that have accelerated because of the COVID-19 pandemic. For example, we can take learnings from the online environment, which represented 59% of our 2020 sales, to the offline environment, which we see as poised for growth at pet specialty stores in 2022. This approach will be under a single banner brand, Halo. |

• | Capitalize on continuing trends of pet humanization. We believe our combination of innovative products designed specifically for certain channels can assist our growth to become a leader in the premium and super-premium categories across dog and cat food. With an average of more than $500 spent annually on pet food per pet owning household and the number of pet owning households increasing, we believe that the super-premium sub-category is poised to be among the fastest growing segments of pet care spending. |

• | Well Positioned to Capitalize On a Once-in-a-Generation Demographic Shift in China. We believe that China represents the largest macro-growth opportunity in the global pet food industry. In China, the number of households that own a pet has doubled in the last five years, with younger pet owners leading growth. Even though the absolute number of Chinese households that own a pet recently surpassed that same figure in the US, only 20% of Chinese households own a pet, compared to 67% in the United States. This has translated to a 28% annual growth rate in the premium dry cat food market, and a 20% annual growth rate in the dry dog food market. In 2020, more than 50% of Chinese consumers that purchased our products were born after 1990, and approximately 80% made those purchases online. |

• | Ability to Pursue Strategic Acquisitions. In 2019, we successfully closed the Halo and TruPet acquisitions. We remain committed to locating the right assets that meet our investment criteria. Through our longstanding industry contacts we are able to source proprietary opportunities and transactions. Our preference is to maintain the asset light business model we currently operate and identify products and brands that are complementary to our existing portfolio. We have a wide scope of systems in place to ensure scalable success and reduce integration risk, including a world class enterprise resource planning or ERP system, NetSuite, a fully scaled and outsourced IT provider (Chelsea Technologies) and a platform to effectively meet public company reporting requirements (Workiva). Furthermore, our public company structure has historically enabled Better Choice to offer transaction consideration in the form of cash and stock. We have a robust pipeline of potential acquisitions which we expect to pursue in the form of pre-process and direct founder dialogue discussions. |

• | restrictions on the marketing or manufacturing of a product; |

• | required modification of promotional materials or issuance of corrective marketing information; |

• | issuance of safety alerts, press releases, or other communications containing warnings or other safety information about a product; |

• | warning or untitled letters; |

• | product seizure or detention; |

• | refusal to permit the import or export of products; |

• | fines, injunctions, or consent decrees; and |

• | imposition of civil or criminal penalties. |

Name | | | Age | | | Position |

Scott Lerner | | | 49 | | | Chief Executive Officer |

Sharla Cook | | | 40 | | | Chief Financial Officer |

Donald Young | | | 57 | | | Executive Vice President, Sales |

Robert Sauermann | | | 29 | | | Executive Vice President, Strategy |

Michael Young | | | 42 | | | Chairman of the Board of Directors |

Jeff D. Davis | | | 60 | | | Director |

Gil Fronzaglia | | | 59 | | | Director |

Lori Taylor | | | 51 | | | Director |

John M. Word III | | | 71 | | | Director |

Name and Principal Position | | | Year(1) | | | Salary ($) | | | Bonus ($) | | | Stock Awards ($) | | | Option Awards ($)(2) | | | Non-Equity Incentive Plan Compensation ($) | | | All Other Compensation ($) | | | Total ($) |

Werner von Pein(3) Chief Executive Officer | | | 2020 | | | $316,712 | | | $103,087 | | | $0 | | | $367,196 | | | $0 | | | $39,175 | | | $826,170 |

Sharla Cook(4) Chief Financial Officer | | | 2020 | | | $143,562 | | | $45,313 | | | $0 | | | $79,721 | | | $0 | | | $3,385 | | | $271,981 |

Damian Dalla-Longa(5) Executive Vice President, Capital Markets and Corporate Development | | | 2020 | | | $291,644 | | | $56,642 | | | $0 | | | $106,571 | | | $0 | | | $0 | | | $454,857 |

| | 2019 | | | $192,857 | | | $100,000 | | | $600,000 | | | $3,572,699 | | | $0 | | | $0 | | | $4,465,556 | ||

Anthony Santarsiero(6) Executive Vice President, Direct to Consumer | | | 2020 | | | $250,000 | | | $56,642 | | | $0 | | | $74,013 | | | $0 | | | $8,414 | | | $389,069 |

| | 2019 | | | $166,047 | | | $25,000 | | | $0 | | | $3,077,101 | | | $0 | | | $5,740 | | | $3,273,888 | ||

Robert Sauermann(7) Executive Vice President, Strategy & Finance | | | 2020 | | | $216,712 | | | $50,977 | | | $0 | | | $56,131 | | | $0 | | | $6,501 | | | $330,321 |

Andreas Schulmeyer(8) Former Chief Financial Officer | | | 2020 | | | $97,945 | | | $0 | | | $5,956 | | | $174,327 | | | $0 | | | $3,556 | | | $281,784 |

| | 2019 | | | $105,769 | | | $0 | | | $0 | | | $1,877,285 | | | $0 | | | $37,011 | | | $2,020,065 |

(1) | Ms. Cook commenced employment with us in April 2020 and was appointed as our Chief Financial Officer in October 2020. Mr. Schulmeyer’s employment with us terminated on May 22, 2020 and Mr. von Pein’s employment terminated on December 31, 2020. |

(2) | The values in this column reflect for 2019 awards the aggregate grant date fair value of the stock option awards and the incremental value due to the repricings on December 19, 2019 and October 1, 2020 as computed in accordance with ASC Topic 718. The value of stock options granted subsequent to October 1, 2020 are based on their aggregate grant date fair values in accordance with ASC Topic 718. See “Note 15 – Share-based compensation” to our audited consolidated financial statements for the year ended December 31, 2020 included in this prospectus for further information on the fair value of stock option awards. |

(3) | Mr. von Pein received (i) $6,297 in car allowance payments, (ii) $2,752 in auto insurance payments (iii) $20,625 in housing allowance payments and (iv) $9,501 in matching 401(k) payments. On December 28, 2020, we entered into an agreement with Mr. von Pein pursuant to which he retired from his role as Chief Executive Officer of the Company effective on December 31, 2020. |

(4) | Ms. Cook received $3,385 in matching 401(k) payments. |

(5) | During 2019, Mr. Dalla-Longa received (i) a signing bonus of $100,000 as per his employment contract with Better Choice, and (ii) an award of 16,667 shares in lieu of the change of control payment contained in his Bona Vida employment contract. On February 5, 2020, Mr. Dalla-Longa resigned as our Chief Executive Officer and was simultaneously appointed to Executive Vice President, Corporate Development. Mr. Dalla-Longa separated from the Company February 8, 2021. |

(6) | During 2020, Mr. Santarsiero received $8,414 in matching 401(k) payments. During 2019, Mr. Santarsiero received (i) a signing bonus of $25,000 as per his employment contract and (ii) $5,740 in matching 401(k) payments. Mr. Santarsiero separated from the Company on February 1, 2021. |

(7) | During 2020, Mr. Sauermann received $6,501 in matching 401(k) payments. |

(8) | During 2020, Mr. Schulmeyer received (i) $5,956 in restricted stock awards for services performed and (ii) $3,556 in matching 401(k) payments. During 2019, Mr. Schulmeyer received (i) $32,876 in compensation for work prior to joining the Company and (ii) $4,135 in matching 401(k) payments. On May 8, 2020, we entered into an agreement with Mr. Schulmeyer pursuant to which he resigned as our Chief Financial Officer effective on May 22, 2020. |

• | “cause” means (i) any act of personal dishonesty taken by the Executive in connection with their responsibilities as an employee which is intended to result in personal enrichment of the Executive, (ii) the Executive’s conviction of a felony that the Board of Directors reasonably believes has had or will have a material detrimental effect on the Company’s reputation or business, (iii) a willful act by the Executive that constitutes misconduct and is injurious to the Company, including without limitation any breach of Section 11 hereof, and (iv) continued willful violations by the Executive of the Executive’s obligations to the Company for a period of thirty (30) days after there has been delivered to the Executive a written demand for performance from the Company which describes the basis for the Company’s belief that the Executive has not substantially performed their duties. |

• | “good reason” shall exist if one or more of the following circumstances exists uncured for a period of thirty (30) days after the Executive has notified the Company of the existence of such circumstance(s) after a merger: (i) without the Executive’s express written consent, a significant reduction of the Executive’s duties, position or responsibilities relative to the Executive’s duties, position or responsibilities in effect immediately prior to such reduction, or the removal of the Executive from such position, duties, and responsibilities, unless the Executive is provided with comparable duties, position and responsibilities, it being understood that the Executive shall not be deemed to have been removed from such position if and as long as the Executive shall be offered or shall have an executive position within their area of experience or expertise; (ii) without the Executive’s express written consent, a substantial reduction, without good business reasons, of the facilities and tools (including office space and location) available to the Executive immediately prior to such reduction; (iii) a reduction by the Company of the Executive’s base salary as in effect immediately prior to such reduction; (iv) a material reduction by the Company in the kind or level of employee benefits to which the Executive is entitled immediately prior to such a reduction with the result that the Executive’s overall benefits package is significantly reduced; or (v) without the Executive’s express written consent, the relocation of the Executive to a facility or a location more than fifty (50) miles from their then-current location. |

Named Executive Officer | | | Annual Base Salary |

Werner von Pein | | | $325,000(1) |

Sharla Cook | | | $200,000 |

Damian Dalla-Longa | | | $250,000(2) |

Anthony Santarsiero | | | $250,000 |

Robert Sauermann | | | $225,000(3) |

Andreas Schulmeyer | | | $250,000 |

(1) | Increased from $300,000 effective May 1, 2020. |

(2) | Decreased from $300,000 effective November 1, 2020. |

(3) | Increased from $200,000 effective May 1, 2020. |

Plan category | | | Number of Securities to be issued upon exercise of outstanding options, warrants and rights | | | Weighted average exercise price of outstanding options, warrants and rights(2) | | | Number of securities remaining available for future issuance under equity compensation plans (excluding securities reflected in column (a)) |

| | | (a) | | | (b) | | | (c) | |

Equity compensation plans approved by stockholders(1) | | | 2,201,293 | | | $6.42 | | | 48,707 |

Total | | | 2,201,293 | | | $6.42 | | | 48,707 |

(1) | The Amended and Restated 2019 Incentive Award Plan provides for an annual increase on the first day of each calendar year beginning on January 1, 2020 and ending on and including January 1, 2029, equal to the lesser of (A) 10% of the shares of common stock outstanding (on an as-converted basis) on the last day of the immediately preceding fiscal year and (B) such smaller number of shares of common stock as determined by the Board. |

| | | Option Awards | |||||||||||||

Name | | | Number of Securities Underlying Unexercised Options (#) Exercisable | | | Number of Securities Underlying Unexercised Options (#) Unexercisable | | | Equity Incentive Plan Awards: Number of Securities Underlying Unexercised Unearned Options (#) | | | Option Exercise Price ($) | | | Option Expiration Date |

Werner von Pein | | | 95,834 | | | (a) | | | — | | | $3.60 | | | (a) |

Sharla A. Cook | | | — | | | —(b) | | | 33,334 | | | $3.60 | | | 4/13/2030 |

Damian Dalla-Longa | | | 158,334 | | | —(c) | | | 50,000 | | | (c) | | | (c) |

Robert Sauermann | | | 22,223 | | | —(d) | | | 61,112 | | | $3.60 | | | (d) |

Anthony Santarsiero | | | 140,278 | | | —(e) | | | 43,056 | | | $3.60 | | | (e) |

(a) | Options to vest as to 1/3rd of the shares on the first anniversary of the grant date and 1/36th of the shares to vest monthly thereafter. Mr. von Pein’s options were granted at various times as shown below: |

• | 100,000 options were issued on December 19, 2019 at $3.60 and expire on December 19, 2029. |

• | 16,667 options were issued on October 8, 2020 at $3.60 and expire on October 8, 2030. |

• | Mr. von Pein retired from the Company on December 28, 2020 at which time 75% of Mr. von Pein’s unvested options became fully vested per the separation agreement by and between the Company and Mr. von Pein. |

(b) | Options to vest as to 1/3rd of the shares on the first anniversary of the grant date and 1/36th of the shares to vest monthly thereafter. Ms. Cook’s options were granted as shown below: |

• | 33,334 options were issued on April 13, 2020 at $3.60. |

(c) | Options to vest as follows: |

• | 200,000 options were issued on May 2, 2019 at $3.60 and expire on May 2, 2029. Options to vest on a monthly basis over a two year period (1/24th of award per month). |

• | 8,334 options were issued on November 1, 2020 at $4.92 and expire on November 1, 2030. Options to vest as to 1/3rd of the shares on the first anniversary of the grant date and 1/36th of the shares to vest monthly thereafter. |

(d) | Options to vest as to 1/3rd of the shares on the first anniversary of the grant date and 1/36th of the shares to vest monthly thereafter. Mr. Sauermann’s options were granted at various times as shown below: |

• | 66,667 options were issued on December 19, 2019 at $3.60 and expire on December 19, 2029. |

• | 16,667 options were issued on October 8, 2020 at $3.60 and expire October 8, 2030. |

(e) | Options to vest as follows: |

• | 166,667 options were issued on May 2, 2019 at $3.60 and expire May 2, 2029. Options to vest on a monthly basis over a two year period (1/24th of award per month). |

• | 16,667 options were issued on December 19, 2019 at $3.60 and expire December 19, 2029. Options to vest on a monthly basis over a two year period (1/24th of award per month). |

Name | | | Fees Earned or Paid in Cash | | | Stock Awards | | | Option Awards(1) | | | Non-equity Incentive Plan Compensation | | | All Other Compensation(2) | | | Total Compensation |

Michael Young | | | $— | | | $— | | | $33,988 | | | $— | | | $— | | | $33,988 |

Jeff Davis | | | $— | | | $— | | | $33,988 | | | $— | | | $— | | | $33,988 |

Michael Close | | | $— | | | $150,000 | | | $— | | | $— | | | $510,469 | | | $660,469 |

Clinton Gee | | | $— | | | $150,000 | | | $— | | | $— | | | $510,469 | | | $660,469 |

Lori Taylor | | | $— | | | $— | | | $78,173 | | | $— | | | $— | | | $78,173 |

John Word | | | $— | | | $150,000 | | | $— | | | $— | | | $— | | | $150,000 |

(1) | The values in this column reflect for 2019 awards the aggregate grant date fair value of the stock option awards and the incremental value due to the repricings on December 19, 2019 and October 1, 2020 as computed in accordance with ASC Topic 718. The value of stock options |

(2) | Includes compensation expense related to warrants issued in connection with the June 2020 Notes and Citizens ABL Facility. See “Note 11 – Warrants” to our audited consolidated financial statements for the year ended December 31, 2020 included in this prospectus for more information. |

Name | | | Options Outstanding at Fiscal Year End |

Michael Young | | | 86,539 |

Jeff Davis | | | 83,334 |

Michael Close | | | — |

Clinton Gee | | | — |

Lori Taylor | | | 191,667 |

John Word | | | — |

| | | Amount and Nature of Beneficial Ownership(1) | ||||

| | | Common Stock | | | % | |

Name of Beneficial Owner | | | | | ||

Holders of More than 5% | | | | | ||

Thriving Paws LLC(2) 750 E Main Street, Suite 600 Stamford, CT 06902 | | | 568,148 | | | 5.1% |

HH-Halo LP(3) 2200 Ross Avenue, 50th Floor Dallas, TX 75201 | | | 554,493 | | | 5.0% |

Edward J. Brown Jr TTEE(4) 20 Boulder View Irvine, CA 92603 | | | 3,816,816 | | | 34.4% |

Directors and Executive Officers | | | | | ||

Scott Lerner(5) | | | 8,000 | | | * |

Donald Young(6) | | | 45,934 | | | * |

Robert Sauermann(7) | | | 115,928 | | | 1.0% |

Sharla Cook(8) | | | 20,556 | | | * |

Michael Young(9) | | | 632,632 | | | 5.7% |

John M. Word III(10) | | | 5,520,453 | | | 49.8% |

Gil Fronzaglia(11) | | | 0 | | | * |

Jeff Davis(12) | | | 83,334 | | | * |

Lori Taylor(13) | | | 1,347,005 | | | 12.1% |

All directors and executive officers as a group (9 persons) | | | 7,773,842 | | | 70.1% |

∗ | Represents less than 1% of the number of shares of our common stock outstanding. |

(1) | Beneficial ownership of shares and percentage ownership are determined in accordance with the SEC’s rules. In calculating the number of shares beneficially owned by an individual or entity and the percentage ownership of that individual or entity, shares underlying options, warrants or restricted stock units held by that individual or entity that are either currently exercisable or exercisable within 60 days from the date hereof are deemed outstanding. These shares, however, are not deemed outstanding for the purpose of computing the percentage ownership of any other individual or entity. Unless otherwise indicated and subject to community property laws where applicable, the individuals and entities named in the table above have sole voting and investment power with respect to all shares of our common stock shown as beneficially owned by them. |

(2) | Includes (i) 314,165 shares of common stock and (ii) 253,984 shares of common stock underlying subordinated convertible notes exercisable within 60 days of June 11, 2021. The holder disclaims beneficial ownership of 51,166 shares of common stock underlying warrants due to beneficial ownership limitations. Thriving Paws, LLC (“Thriving Paws”) is controlled by Pegasus Partners III, L.P. (“PP III”). PP III is managed by Pegasus Capital Advisors III, L.P. (“PCA III”), which is controlled, indirectly, by Craig Cogut. As a result of the foregoing, each of Mr. Cogut, PCA III and PP III may be deemed to have beneficial ownership (as determined under Section 13(d) of the Securities Exchange Act of 1934, as amended) of the shares of common stock beneficially owned by Thriving Paws. |

(3) | Includes (i) 38,830 shares of common stock and (ii) 515,663 shares of common stock underlying subordinated convertible notes exercisable within 60 days of June 11, 2021. The holder disclaims beneficial ownership of 103,882 shares of common stock underlying warrants due to beneficial ownership limitations. Thomas O. Hicks is the managing member of HEP Partners LLC, which is the investment manager of HH-Halo LP (“HH-Halo”), and consequently has voting control and investment discretion over securities held by HH-Halo. Mack H. Hicks is the manager of HH-Halo GP LLC, which is the general partner of HH-Halo GP LP, the general partner of HH-Halo. As a result of the foregoing, each of Thomas O. Hicks and Mack H. Hicks may be deemed to have beneficial ownership (as determined under Section 13(d) of the Securities Exchange Act of 1934, as amended) of the shares of common stock beneficially owned by HH-Halo. Each of Thomas O. Hicks and Mack H. Hicks disclaims beneficial ownership of such shares. |

(4) | Includes (i) 130,000 shares of common stock, (ii) 255,899 shares of common stock underlying subordinated convertible notes exercisable within 60 days of June 11, 2021, (iii) 1,764,250 shares of common stock underlying warrants exercisable within 60 days of June 11, 2021 and (iv) 1,666,667 shares of common stock underlying preferred stock convertible within 60 days of June 11, 2021. Edward Brown may be deemed to have beneficial ownership of such shares. |

(5) | Includes (i) 4,000 shares of common stock and (ii) 4,000 shares of common stock underlying warrants exercisable within 60 days of June 11, 2021. |

(6) | Includes (i) 35,934 shares of common stock and (ii) 10,000 shares of common stock underlying warrants exercisable within 60 days of June 11, 2021. |

(7) | Includes (i) 3,334 shares of common stock, (ii) 37,870 shares of common stock underlying warrants exercisable within 60 days of June 11, 2021, (iii) 33,334 shares of common stock underlying preferred stock convertible within 60 days of June 11, 2021, (iv) 6,207 shares of common stock underlying subordinated convertible notes exercisable within 60 days of June 11, 2021 and (v) 35,186 shares of common stock underlying options exercisable within 60 days of June 11, 2021. |

(8) | Includes (i) 3,334 shares of common stock underlying warrants exercisable within 60 days of June 11, 2021, (ii) 3,334 shares of common stock underlying preferred stock convertible within 60 days of June 11, 2021 and 13,889 shares of common stock underlying options exercisable within 60 days of June 11, 2021. |

(9) | Includes (i) 526,927 shares of common stock, (ii) 86,539 shares of common stock underlying options exercisable within 60 days of June 11, 2021, (iii) 19,167 shares of common stock held by Cottingham Capital Partners LLC, which is managed by Mr. Young. Mr. Young disclaims beneficial ownership of (i) 60,834 shares of common stock underlying warrants due to beneficial ownership limitations. |

(10) | Includes (i) 901,138 shares of common stock, (ii) 255,899 shares of common stock underlying subordinated convertible notes exercisable within 60 days of June 11, 2021, (iii) 2,696,750 shares of common stock underlying warrants exercisable within 60 days of June 11, 2021 and (iv) 1,666,667 shares of common stock underlying preferred stock convertible within 60 days of June 11, 2021. |

(11) | Mr. Fronzaglia has 13,334 shares of common stock underlying options outstanding, none of which are exercisable within 60 days of June 11, 2021 |

(12) | Includes (i) 83,334 shares of common stock underling options exercisable within 60 days of June 11, 2021. |

(13) | Includes (i) 938,672 shares of common stock held directly by Blue Sky Holdings Trust which are beneficially owned by Lori Taylor, (ii) 191,667 shares of common stock underlying options exercisable within 60 days of June 11, 2021 held directly by Ms. Taylor and (iii) 216,667 shares of common stock underlying warrants held directly by Ms. Taylor. Ms. Taylor is the trustee, compliance officer, and protector of Blue Sky Holdings Trust. |

• | any person who is, or at any time during the applicable period was, one of our executive officers, one of our directors, or a nominee to become one of our directors; |

• | any person who is known by us to be the beneficial owner of more than 5.0% of any class of our voting securities; |

• | any immediate family member of any of the foregoing persons, which means any child, stepchild, parent, stepparent, spouse, sibling, mother-in-law, father-in-law, son-in-law, daughter-in-law, brother-in-law or sister-in-law of a director, executive officer or a beneficial owner of more than 5.0% of any class of our voting securities, and any person (other than a tenant or employee) sharing the household of such director, executive officer or beneficial owner of more than 5.0% of any class of our voting securities; and |

• | any firm, corporation or other entity in which any of the foregoing persons is employed or is a general partner or principal or in a similar position or in which such person has a 5% or greater beneficial ownership interest in any class of the Company’s voting securities. |

• | 200,000,000 shares of common stock, $0.001 par value per share; and |

• | 4,000,000 shares of preferred stock, $0.001 par value per share, of which 30,000 shares are designated as of Series F Preferred Stock preferred stock. |

• | for any breach of their duty of loyalty to us or our stockholders; |

• | for acts or omissions not in good faith or which involve intentional misconduct or a knowing violation of law; |

• | for unlawful payment of dividend or unlawful stock repurchase or redemption, as provided under Section 174 of the DGCL; or |

• | for any transaction from which the director derived an improper personal benefit. |

• | beginning on the date of this prospectus, all [ ] shares of our common stock sold in this offering will be immediately available for sale in the public market; and |

• | beginning 181 days after the date of this prospectus, approximately [ ] additional shares of common stock may become eligible for sale in the public market upon the satisfaction of certain conditions as set forth in the section titled “Lock-Up Agreements” and the volume and other restrictions of Rule 144, as described below. |

• | 1% of the number of shares of our common stock then outstanding, which will equal approximately shares immediately after completion of this offering; or |

• | the average weekly trading volume in our common stock on the NYSE American during the four calendar weeks preceding the filing of a notice on Form 144 with respect to such a sale. |

• | Registration Rights Agreement, dated May 6, 2019, by and among the Company and the persons listed on the signature pages thereto in connection with the May 2019 private placement, as amended by that certain First Amendment to Registration Rights Agreement, dated June 10, 2019, by and among the Company and the stockholders party thereto; |

• | Registration Rights Agreement, dated as of May 6, 2019, by and among Better Choice Company Inc. and the former stockholders of Bona Vida listed on the signature pages thereto; |

• | Registration Rights Agreement, dated as of May 6, 2019, by and among Better Choice Company Inc. and the former member of TruPet listed on the signature pages thereto; |

• | Registration Rights Agreement by and among the Company and the persons listed on the signature pages thereto in connection with the November 2019 private placement; |

• | Registration Rights Agreement by and among the Company and the persons listed on the signature pages thereto in connection with the June 2020 private placement; |

• | Registration Rights Agreement by and among the Company and the persons listed on the signature pages thereto in connection with the October 2020 Series F Private Placement, as amended by that certain First Amendment to Registration Rights Agreement; and |

• | Registration Rights Agreement by and among the Company and the persons listed on the signature pages thereto in connection with the January 2021 Private Placement. |

| | | Number of Shares | |

D.A. Davidson & Co. | | | |

Roth Capital Partners, LLC | | | |

| | | ||

Total | | |

• | our results of operations; |

• | our current financial condition; |

• | our future prospects; |

• | our management; |

• | recently quoted prices of our common stock on OTCQX; |

• | the economic conditions in and future prospects for the industry in which we compete; and |

• | other factors we and the representative deem relevant. |

| | | Total Per Share | | | Without Option to Purchase Additional Shares | | | With Option to Purchase Additional Shares | |

Initial public offering price | | | | | | | |||

Underwriting discounts and commissions | | | | | | | |||

Proceeds, before estimated expenses, to us | | | | | | |

a. | to any legal entity which is a qualified investor as defined under the Prospectus Regulation; |

b. | to fewer than 150 natural or legal persons (other than qualified investors as defined under the Prospectus Regulation), subject to obtaining the prior consent of the underwriter for any such offer; or |

c. | in any other circumstances falling within Article 1(4) of the Prospectus Regulation, |

a. | to any legal entity which is a qualified investor as defined under the UK Prospectus Regulation; |

b. | to fewer than 150 natural or legal persons (other than qualified investors as defined under the UK Prospectus Regulation), subject to obtaining the prior consent of underwriter for any such offer; or |

c. | at any time in other circumstances falling within section 86 of the FSMA, |

| | | Page | |

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | |

| | | Page | |

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | |

| | | March 31, 2021 Unaudited | | | December 31, 2020 Audited | |

Assets | | | | | ||

Cash and cash equivalents | | | $4,298 | | | $3,926 |

Restricted cash | | | 63 | | | 63 |

Accounts receivable, net | | | 6,675 | | | 4,631 |

Inventories, net | | | 4,582 | | | 4,869 |

Prepaid expenses and other current assets | | | 4,258 | | | 4,074 |

Total Current Assets | | | 19,876 | | | 17,563 |

Property and equipment, net | | | 205 | | | 252 |

Right-of-use assets, operating lease | | | 305 | | | 345 |

Intangible assets, net | | | 12,732 | | | 13,115 |

Goodwill | | | 18,614 | | | 18,614 |

Other assets | | | 635 | | | 1,364 |

Total Assets | | | $52,367 | | | $51,253 |

Liabilities & Stockholders’ Deficit | | | | | ||

Current Liabilities | | | | | ||

Term loans, net | | | $628 | | | $7,826 |

PPP loans | | | 315 | | | 190 |

Other liabilities | | | 41 | | | 47 |

Accounts payable | | | 5,221 | | | 3,137 |

Accrued liabilities | | | 2,090 | | | 3,003 |

Deferred revenue | | | 257 | | | 350 |

Operating lease liability | | | 180 | | | 173 |

Warrant liabilities | | | 46,333 | | | 39,850 |

Total Current Liabilities | | | 55,065 | | | 54,576 |

Non-current Liabilities | | | | | ||

Notes payable, net | | | 19,609 | | | 18,910 |

Term loans, net | | | 5,219 | | | — |

Lines of credit, net | | | 4,781 | | | 5,023 |

PPP loans | | | 537 | | | 662 |

Operating lease liability | | | 136 | | | 184 |

Total Non-current Liabilities | | | 30,282 | | | 24,779 |

Total Liabilities | | | 85,347 | | | 79,355 |

Stockholders’ Deficit | | | | | ||

Common stock, $0.001 par value, 200,000,000 shares authorized, 66,004,348 and 51,908,398 shares issued and outstanding as of March 31, 2021 and December 31, 2020, respectively | | | 66 | | | 52 |

Series F Preferred Stock, $0.001 par value, 30,000 shares authorized, 17,306 and 21,754 shares issued and outstanding as of March 31, 2021 and December 31, 2020, respectively | | | — | | | — |

Additional paid-in capital | | | 240,847 | | | 232,487 |

Accumulated deficit | | | (273,893) | | | (260,641) |

Total Stockholders’ Deficit | | | (32,980) | | | (28,102) |

Total Liabilities and Stockholders’ Deficit | | | $52,367 | | | $51,253 |

| | | Three Months Ended March 31, | ||||

| | | 2021 | | | 2020 | |

Net sales | | | $10,830 | | | $12,226 |

Cost of goods sold | | | 6,556 | | | 8,069 |

Gross profit | | | 4,274 | | | 4,157 |

Operating expenses: | | | | | ||

General and administrative | | | 4,551 | | | 8,245 |

Share-based compensation | | | 2,525 | | | 2,485 |

Sales and marketing | | | 2,336 | | | 1,959 |

Total operating expenses | | | 9,412 | | | 12,689 |

Loss from operations | | | (5,138) | | | (8,532) |

Other expense (income): | | | | | ||

Interest expense | | | 835 | | | 2,301 |

Loss on extinguishment of debt | | | 394 | | | — |

Change in fair value of warrant liabilities | | | 6,483 | | | (1,379) |

Total other expense, net | | | 7,712 | | | 922 |

Net and comprehensive loss | | | (12,850) | | | (9,454) |

Preferred dividends | | | — | | | 34 |

Net and comprehensive loss available to common stockholders | | | $(12,850) | | | $(9,488) |

Weighted average number of shares outstanding, basic and diluted | | | 57,525,054 | | | 48,526,396 |

Loss per share, basic and diluted | | | $(0.23) | | | $(0.20) |

| | | Common Stock | | | Series F Convertible Preferred Stock | | | Additional paid-in capital | | | Accumulated deficit | | | Total Stockholders’ Deficit | |||||||

| | | Shares | | | Amount | | | Shares | | | Amount | | |||||||||

Balance as of December 31, 2020 | | | 51,908,398 | | | $52 | | | 21,754 | | | $— | | | $232,487 | | | $(260,641) | | | $(28,102) |

Shares and warrants issued pursuant to private placement | | | 3,280,400 | | | 3 | | | — | | | — | | | 4,069 | | | — | | | 4,072 |

Share-based compensation | | | 105,222 | | | — | | | — | | | — | | | 2,544 | | | — | | | 2,544 |

Warrant exercises | | | 1,784,298 | | | 2 | | | — | | | — | | | 1,308 | | | — | | | 1,310 |

Shares issued to third-party for services | | | 30,000 | | | — | | | — | | | — | | | 46 | | | — | | | 46 |

Warrant modifications | | | — | | | — | | | — | | | 402 | | | (402) | | | — | | | |

Conversion of Series F shares to common stock | | | 8,896,030 | | | 9 | | | (4,448) | | | — | | | (9) | | | — | | | — |

Net and comprehensive loss available to common stockholders | | | — | | | — | | | — | | | — | | | — | | | (12,850) | | | (12,850) |

Balance as of March 31, 2021 | | | 66,004,348 | | | $66 | | | 17,306 | | | $— | | | $240,847 | | | $(273,893) | | | $(32,980) |

| | | Common Stock | | | Additional Paid-In Capital | | | Accumulated Deficit | | | Total Stockholders’ Deficit | | | Redeemable Series E Convertible Preferred Stock | |||||||

| | | Shares | | | Amount | | | Shares | | | Amount | ||||||||||

Balance as of December 31, 2019 | | | 47,977,390 | | | $48 | | | $194,150 | | | $(201,269) | | | $(7,071) | | | 1,387,378 | | | $10,566 |

Shares issued pursuant to a private placement | | | 308,642 | | | — | | | 500 | | | — | | | 500 | | | — | | | — |

Share-based compensation | | | 455,956 | | | 1 | | | 2,484 | | | — | | | 2,485 | | | — | | | — |

Shares and warrants issued to third party for contract termination | | | 72,720 | | | — | | | 198 | | | — | | | 198 | | | — | | | — |

Shares issued to third parties for services | | | 125,000 | | | — | | | 125 | | | — | | | 125 | | | — | | | — |

Warrants issued to third parties for services | | | — | | | — | | | 2,594 | | | — | | | 2,594 | | | — | | | — |

Net and comprehensive loss available to common stockholders | | | — | | | — | | | — | | | (9,488) | | | (9,488) | | | — | | | — |

Balance as of March 31, 2020 | | | 48,939,708 | | | $49 | | | $200,051 | | | $(210,757) | | | $(10,657) | | | 1,387,378 | | | $10,566 |

| | | Three Months Ended March 31, | ||||

| | | 2021 | | | 2020 | |

Cash Flow from Operating Activities: | | | | | ||

Net and comprehensive loss available to common stockholders | | | $(12,850) | | | $(9,488) |

Adjustments to reconcile net and comprehensive loss to net cash used in operating activities: | | | | | ||

Shares and warrants issued to third parties for services | | | 46 | | | 2,792 |

Depreciation and amortization | | | 411 | | | 457 |

Amortization of debt issuance costs and discounts | | | 161 | | | 1,090 |

Share-based compensation | | | 2,544 | | | 2,485 |

Change in fair value of warrant liabilities | | | 6,483 | | | (1,379) |

Payment In Kind (PIK) interest expense on notes payable | | | 548 | | | 459 |

Other | | | (92) | | | 644 |

Changes in operating assets and liabilities: | | | | | ||

Accounts receivable, net | | | (2,044) | | | (297) |